Multiple Linear Regression in R: Simple & Stepwise with Examples

⚡ Smart Summary

Simple and Multiple Linear Regression in R model a continuous outcome as a weighted sum of predictors fitted by ordinary least squares. This walkthrough covers lm(), coefficient reading, factor predictors, residual diagnostics, prediction, and automatic variable selection.

Where Linear Regression Fits in Machine Learning

Linear regression is one of the oldest supervised machine learning algorithms, and it is still the first model most analysts reach for. One of the earliest machine learning applications was the spam filter.

Other common applications of machine learning include:

- Identification of unwanted spam messages in email

- Segmentation of customer behavior for targeted advertising

- Reduction of fraudulent credit card transactions

- Optimization of energy use in homes and office buildings

- Facial recognition

Supervised Learning

In Supervised Learning, the training data you feed to the algorithm includes a label.

Classification is probably the most used supervised learning technique. One of the first classification tasks researchers tackled was the spam filter. The objective of the learning is to predict whether an email is classified as spam or ham (good email). The machine, after the training step, can detect the class of email.

Regressions are commonly used in the machine learning field to predict continuous value. A regression task can predict the value of a dependent variable based on a set of independent variables (also called predictors or regressors). For instance, linear regressions can predict a stock price, weather forecast, sales and so on.

Some fundamental supervised learning algorithms are:

- Linear regression

- Logistic regression

- Nearest Neighbors

- Support Vector Machine (SVM)

- Decision trees and Random Forest

- Neural Networks

Unsupervised Learning

In Unsupervised Learning, the training data is unlabeled. The system tries to learn without a reference. Below is a list of unsupervised learning algorithms.

- K-mean

- Hierarchical Cluster Analysis

- Expectation Maximization

- Visualization and dimensionality reduction

- Principal Component Analysis

- Kernel PCA

- Locally-Linear Embedding

With that context in place, the rest of this tutorial builds regression models in R step by step.

Simple Linear Regression in R

Linear regression answers a simple question: can you measure an exact relationship between one target variable and a set of predictors?

The simplest probabilistic model is the straight-line model:

![]()

where

- y = Dependent variable

- x = Independent variable

-

= random error component

= random error component -

= intercept

= intercept -

= Coefficient of x

= Coefficient of x

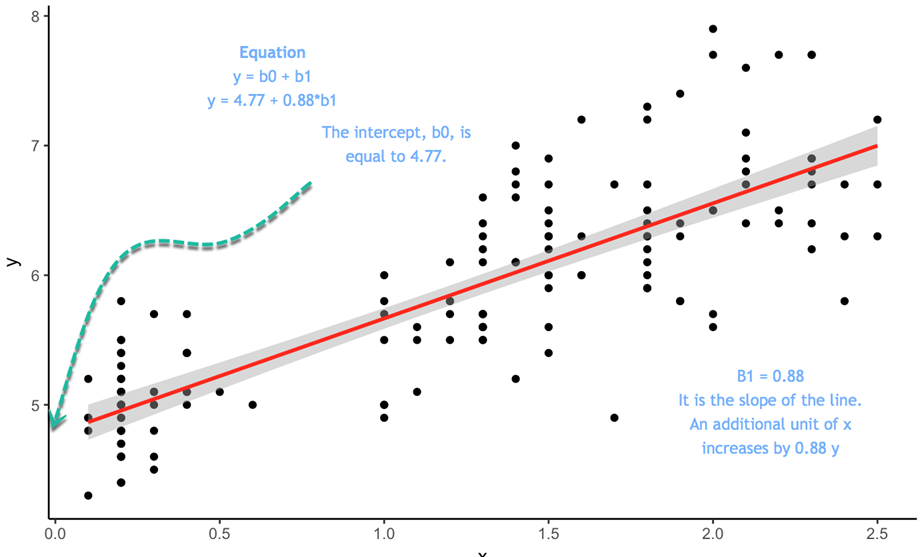

Consider the following plot:

The equation is ![]() In this equation the intercept is 4.77, so when x equals 0 the fitted value of y is 4.77. The slope tells you in which proportion y varies when x varies.

In this equation the intercept is 4.77, so when x equals 0 the fitted value of y is 4.77. The slope tells you in which proportion y varies when x varies.

To estimate the optimal values of ![]() and

and ![]() , you use a method called Ordinary Least Squares (OLS). This method tries to find the parameters that minimize the sum of the squared errors, that is the vertical distance between the predicted y values and the actual y values. The difference is known as the error term.

, you use a method called Ordinary Least Squares (OLS). This method tries to find the parameters that minimize the sum of the squared errors, that is the vertical distance between the predicted y values and the actual y values. The difference is known as the error term.

Before you estimate the model, you can determine whether a linear relationship between y and x is plausible by plotting a scatterplot.

Scatterplot

We will use a very simple dataset to explain the concept of simple linear regression. We will import the Average Heights and weights for American Women. The dataset contains 15 observations. You want to measure whether Heights are positively correlated with weights.

library(ggplot2) path <- 'https://raw.githubusercontent.com/guru99-edu/R-Programming/master/women.csv' df <-read.csv(path) ggplot(df,aes(x=height, y = weight))+ geom_point()

Output:

The scatterplot suggests a general tendency for weight to increase as height increases. In the next step, you will measure by how much weight increases for each additional unit of height.

Least Squares Estimates

In a simple OLS regression, the computation of ![]() and

and ![]() is straightforward. This tutorial does not derive the formulas, it only states them.

is straightforward. This tutorial does not derive the formulas, it only states them.

You want to estimate: ![]()

The goal of the OLS regression is to minimize the following equation:

![]()

where

![]() is the actual value and

is the actual value and ![]() is the predicted value.

is the predicted value.

The solution for ![]() is

is ![]()

Note that ![]() means the average value of x

means the average value of x

The solution for ![]() is

is ![]()

In R, you can use the cov() and var() functions to estimate ![]() and you can use the mean() function to estimate

and you can use the mean() function to estimate ![]()

beta <- cov(df$height, df$weight) / var (df$height) beta

Output:

##[1] 3.45

alpha <- mean(df$weight) - beta * mean(df$height) alpha

Output:

## [1] -87.51667

The beta coefficient implies that for each additional inch of height, the average weight increases by 3.45 pounds.

Estimating a linear equation by hand is instructive but impractical. R provides the lm() function to do it for you, and you will use it from the next section onward. In real projects you will almost never fit a single-predictor model; regression tasks normally involve many estimators at once.

Multiple Linear Regression in R

Practical applications of regression analysis use models more complex than the simple straight-line model. The probabilistic model that includes more than one independent variable is called multiple regression models. The general form of this model is:

![]()

In matrix notation, you can rewrite the model:

The dependent variable y is now a function of k independent variables. The value of the coefficient ![]() determines the contribution of the independent variable

determines the contribution of the independent variable ![]() and

and ![]() .

.

We briefly introduce the assumption we made about the random error ![]() of the OLS:

of the OLS:

- Mean equal to 0

- Variance equal to

- Normal distribution

- Random errors are independent (in a probabilistic sense)

You need to solve for ![]() , the vector of regression coefficients that minimise the sum of the squared errors between the predicted and actual y values.

, the vector of regression coefficients that minimise the sum of the squared errors between the predicted and actual y values.

The closed-form solution is:

![]()

with:

- indicates the transpose of the matrix X

indicates the invertible matrix

indicates the invertible matrix

The examples below use the built-in mtcars dataset. The goal is to predict miles per gallon (mpg) from a set of features.

Continuous Variables in R

For now, you will only use the continuous variables and put aside categorical features. The variable am is a binary variable taking the value of 1 if the transmission is manual and 0 for automatic cars; vs is also a binary variable.

library(dplyr) df <- mtcars %>% select(-c(am, vs, cyl, gear, carb)) glimpse(df)

Output:

## Observations: 32 ## Variables: 6 ## $ mpg <dbl> 21.0, 21.0, 22.8, 21.4, 18.7, 18.1, 14.3, 24.4, 22.8, 19.... ## $ disp <dbl> 160.0, 160.0, 108.0, 258.0, 360.0, 225.0, 360.0, 146.7, 1... ## $ hp <dbl> 110, 110, 93, 110, 175, 105, 245, 62, 95, 123, 123, 180, ... ## $ drat <dbl> 3.90, 3.90, 3.85, 3.08, 3.15, 2.76, 3.21, 3.69, 3.92, 3.9... ## $ wt <dbl> 2.620, 2.875, 2.320, 3.215, 3.440, 3.460, 3.570, 3.190, 3... ## $ qsec <dbl> 16.46, 17.02, 18.61, 19.44, 17.02, 20.22, 15.84, 20.00, 2...

You can use the lm() function to compute the parameters. The basic syntax of this function is:

lm(formula, data, subset)

Arguments:

-formula: The equation you want to estimate

-data: The dataset used

-subset: Estimate the model on a subset of the dataset

Remember an equation is of the following form

![]()

in R

- The symbol = is replaced by ~

- Each x is replaced by the variable name

- If you want to drop the constant, add -1 at the end of the formula

Example:

You want to estimate the weight of individuals based on their height and revenue. The equation is

![]()

The equation in R is written as follow:

y ~ X1+ X2+…+Xn # With intercept

So for our example:

- Weigh ~ height + revenue

Your objective is to estimate the mile per gallon based on a set of variables. The equation to estimate is:

![]()

You will estimate your first linear regression and store the result in the fit object.

model <- mpg ~ disp + hp + drat + wt + qsec

fit <- lm(model, df)

fit

Code Explanation

- model <- mpg ~ disp + hp + drat + wt + qsec: Store the model to estimate

- lm(model, df): Estimate the model with the data frame df

## ## Call: ## lm(formula = model, data = df) ## ## Coefficients: ## (Intercept) disp hp drat wt ## 16.53357 0.00872 -0.02060 2.01577 -4.38546 ## qsec ## 0.64015

The output does not provide enough information about the quality of the fit. You can access more details such as the significance of the coefficients, the degree of freedom and the shape of the residuals with the summary() function.

summary(fit)

Output:

## return the p-value and coefficient ## ## Call: ## lm(formula = model, data = df) ## ## Residuals: ## Min 1Q Median 3Q Max ## -3.5404 -1.6701 -0.4264 1.1320 5.4996 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 16.53357 10.96423 1.508 0.14362 ## disp 0.00872 0.01119 0.779 0.44281 ## hp -0.02060 0.01528 -1.348 0.18936 ## drat 2.01578 1.30946 1.539 0.13579 ## wt -4.38546 1.24343 -3.527 0.00158 ** ## qsec 0.64015 0.45934 1.394 0.17523 ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 2.558 on 26 degrees of freedom ## Multiple R-squared: 0.8489, Adjusted R-squared: 0.8199 ## F-statistic: 29.22 on 5 and 26 DF, p-value: 6.892e-10

Inference from the above table output

- The table shows a strong negative relationship between wt and mpg, and a positive coefficient for drat.

- Only the variable wt has a statistical impact on mpg. Remember, to test a hypothesis in statistic, we use:

- H0: No statistical impact

- H1: The predictor has a meaningful impact on y

- If the p value is lower than 0.05, it indicates the variable is statistically significant

- Adjusted R-squared: the share of the variance of y explained by the model, corrected for the number of predictors. Here it is 0.8199, so the model explains about 82 percent of the variance of mpg. R-squared always sits between 0 and 1, and higher is better.

You can run the ANOVA test to estimate the effect of each feature on the variances with the anova() function.

anova(fit)

Output:

## Analysis of Variance Table ## ## Response: mpg ## Df Sum Sq Mean Sq F value Pr(>F) ## disp 1 808.89 808.89 123.6185 2.23e-11 *** ## hp 1 33.67 33.67 5.1449 0.031854 * ## drat 1 30.15 30.15 4.6073 0.041340 * ## wt 1 70.51 70.51 10.7754 0.002933 ** ## qsec 1 12.71 12.71 1.9422 0.175233 ## Residuals 26 170.13 6.54 ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

A more conventional way to estimate the model performance is to display the residual against different measures.

You can use the plot() function to show four graphs:

– Residuals vs Fitted values

– Normal Q-Q plot: Theoretical Quartile vs Standardized residuals

– Scale-Location: Fitted values vs Square roots of the standardised residuals

– Residuals vs Leverage: Leverage vs Standardized residuals

You add the code par(mfrow = c(2, 2)) before plot(fit). If you don’t add this line of code, R prompts you to hit the enter command to display the next graph.

par(mfrow = c(2, 2))

Code Explanation

- (mfrow=c(2,2)): return a window with the four graphs side by side.

- The first 2 adds the number of rows

- The second 2 adds the number of columns.

- If you write (mfrow=c(3,2)): you will create a 3 rows 2 columns window

plot(fit)

Output:

The lm() formula returns a list containing a lot of useful information. You can access them with the fit object you have created, followed by the $ sign and the information you want to extract.

– coefficients: `fit$coefficients`

– residuals: `fit$residuals`

– fitted value: `fit$fitted.values`

Factors Regression in R

In the last model estimation, you regress mpg on continuous variables only. It is straightforward to add factor variables to the model. You add the variable am to your model. It is important to be sure the variable is a factor level and not continuous.

df <- mtcars %>%

mutate(cyl = factor(cyl),

vs = factor(vs),

am = factor(am),

gear = factor(gear),

carb = factor(carb))

model <- mpg ~ .

summary(lm(model, df))

Output:

## ## Call: ## lm(formula = model, data = df) ## ## Residuals: ## Min 1Q Median 3Q Max ## -3.5087 -1.3584 -0.0948 0.7745 4.6251 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 23.87913 20.06582 1.190 0.2525 ## cyl6 -2.64870 3.04089 -0.871 0.3975 ## cyl8 -0.33616 7.15954 -0.047 0.9632 ## disp 0.03555 0.03190 1.114 0.2827 ## hp -0.07051 0.03943 -1.788 0.0939 . ## drat 1.18283 2.48348 0.476 0.6407 ## wt -4.52978 2.53875 -1.784 0.0946 . ## qsec 0.36784 0.93540 0.393 0.6997 ## vs1 1.93085 2.87126 0.672 0.5115 ## am1 1.21212 3.21355 0.377 0.7113 ## gear4 1.11435 3.79952 0.293 0.7733 ## gear5 2.52840 3.73636 0.677 0.5089 ## carb2 -0.97935 2.31797 -0.423 0.6787 ## carb3 2.99964 4.29355 0.699 0.4955 ## carb4 1.09142 4.44962 0.245 0.8096 ## carb6 4.47757 6.38406 0.701 0.4938 ## carb8 7.25041 8.36057 0.867 0.3995 ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 2.833 on 15 degrees of freedom ## Multiple R-squared: 0.8931, Adjusted R-squared: 0.779 ## F-statistic: 7.83 on 16 and 15 DF, p-value: 0.000124

R uses the first factor level as a base group. You need to compare the coefficients of the other group against the base group.

Assumptions of Linear Regression in R

Ordinary least squares only produces trustworthy coefficients and p-values when five conditions hold. The four diagnostic plots produced by plot(fit) exist precisely to check them.

- Linearity: the relationship between each predictor and y is linear. Check the Residuals vs Fitted plot; a visible curve means you need a transformation or a polynomial term.

- Independence: the error terms are uncorrelated. Time-ordered data often violates this, which you can test with durbinWatsonTest() from the car package.

- Homoscedasticity: the error variance is constant across fitted values. A funnel shape in the Scale-Location plot signals a violation.

- Normality of residuals: the errors follow a normal distribution. Points should sit on the diagonal of the Normal Q-Q plot.

- No multicollinearity: predictors are not near-duplicates of each other. A variance inflation factor above 5 is the usual warning line.

library(car) vif(fit) # variance inflation factors shapiro.test(residuals(fit)) # normality of residuals

Violations do not always invalidate a model, but they change how confident you can be in the p-values, so check them before reporting any coefficient.

How to Make Predictions with a Linear Regression Model in R

Fitting a model is only half the job. The predict() function applies the fitted coefficients to new observations.

predict(object, newdata, interval = "none", level = 0.95) arguments: -object: The model returned by lm() -newdata: A data frame whose columns match the predictors used in the formula -interval: "none", "confidence" for the mean response, or "prediction" for a single new case -level: The confidence level, 0.95 by default

Follow these three steps.

- Build a data frame of new cases. The column names must match the predictor names in the formula exactly, and factor levels must match the training data.

- Call predict(). Pass the fitted object and the new data frame.

- Add an interval. Choose “confidence” when you want the uncertainty around the average response, and “prediction” when you want the range for one individual car.

new_cars <- data.frame(wt = c(2.5, 3.2), hp = c(110, 175)) fit_final <- lm(mpg ~ wt + hp, data = mtcars) predict(fit_final, newdata = new_cars) predict(fit_final, newdata = new_cars, interval = "prediction")

Reading the result. A car weighing 2.5 thousand pounds with 110 horsepower is predicted at roughly 24.1 mpg. The prediction interval is always wider than the confidence interval, because it carries the uncertainty of a single observation on top of the uncertainty of the fitted line.

Two rules keep predictions honest. Never extrapolate beyond the range of the training predictors, because the straight line has no evidence out there. And always evaluate on data the model has not seen, otherwise the reported error is optimistic.

Linear Regression vs Logistic Regression in R

Analysts often reach for lm() when the outcome is not continuous. The table below shows where the boundary lies.

| Criteria | Linear Regression | Logistic Regression |

|---|---|---|

| Response variable | Continuous | Binary or categorical |

| Predicted output | Any real number | A probability between 0 and 1 |

| Estimation | Ordinary least squares | Maximum likelihood |

| Fit measure | R-squared, RMSE | AIC, deviance, accuracy |

| R function | lm(formula, data) | glm(formula, data, family = “binomial”) |

If the outcome is a yes or no decision, move to the generalized linear model instead of forcing a straight line through zeros and ones.

Stepwise Linear Regression in R

The last part of this tutorial deals with the stepwise regression algorithm. The purpose of this algorithm is to add and remove potential candidates in the models and keep those who have a significant impact on the dependent variable. This algorithm is meaningful when the dataset contains a large list of predictors. You don’t need to manually add and remove the independent variables. The stepwise regression is built to select the best candidates to fit the model.

Let’s see in action how it works. You use the mtcars dataset with the continuous variables only for pedagogical illustration. Before you begin the analysis, it is good practice to inspect the relationships in the data with a correlation matrix. The GGally library is an extension of ggplot2.

The library includes different functions to show summary statistics such as correlation and distribution of all the variables in a matrix. We will use the ggscatmat function, but you can refer to the vignette for more information about the GGally library.

The basic syntax for ggscatmat() is:

ggscatmat(df, columns = 1:ncol(df), corMethod = "pearson") arguments: -df: A matrix of continuous variables -columns: Pick up the columns to use in the function. By default, all columns are used -corMethod: Define the function to compute the correlation between variable. By default, the algorithm uses the Pearson formula

You display the correlation for all your variables and decide which ones are the best candidates for the first step of the stepwise regression. There are some strong correlations between your variables and the dependent variable, mpg.

library(GGally) df <- mtcars %>% select(-c(am, vs, cyl, gear, carb)) ggscatmat(df, columns = 1: ncol(df))

Output:

Stepwise Regression Step by Step Example

Variable selection is an important part of fitting a model, and stepwise regression performs that search automatically. To estimate how many possible choices there are in the dataset, you compute ![]() with k is the number of predictors. The amount of possibilities grows bigger with the number of independent variables. That’s why you need to have an automatic search.

with k is the number of predictors. The amount of possibilities grows bigger with the number of independent variables. That’s why you need to have an automatic search.

You need to install the olsrr package from CRAN. The package is not available yet in Anaconda. Hence, you install it directly from the command line:

install.packages("olsrr")

You can plot all the subsets of possibilities with the fit criteria (i.e. R-square, Adjusted R-square, Bayesian criteria). The model with the lowest AIC criteria will be the final model.

library(olsrr) model <- mpg~. fit <- lm(model, df) test <- ols_all_subset(fit) plot(test)

Code Explanation

- mpg ~.: Construct the model to estimate

- lm(model, df): Run the OLS model

- ols_all_subset(fit): Construct the graphs with the relevant statistical information

- plot(test): Plot the graphs

Output:

Linear regression models use the t-test to estimate the statistical impact of an independent variable on the dependent variable. Researchers commonly set the maximum threshold at 10 percent, and lower p-values indicate a stronger statistical link. Stepwise regression is built around this test to add and remove candidate predictors. The algorithm works as follows:

- Step 1: Regress each predictor on y separately. Namely, regress x_1 on y, x_2 on y to x_n. Store the p-value and keep the regressor with a p-value lower than a defined threshold (0.1 by default). The predictors with a significance lower than the threshold will be added to the final model. If no variable has a p-value lower than the entering threshold, then the algorithm stops, and you have your final model with a constant only.

- Step 2: Use the predictor with the lowest p-value and adds separately one variable. You regress a constant, the best predictor of step one and a third variable. You add to the stepwise model, the new predictors with a value lower than the entering threshold. If no variable has a p-value lower than 0.1, then the algorithm stops, and you have your final model with one predictor only. You regress the stepwise model to check the significance of the step 1 best predictors. If it is higher than the removing threshold, you keep it in the stepwise model. Otherwise, you exclude it.

- Step 3: You replicate step 2 on the new best stepwise model. The algorithm adds predictors to the stepwise model based on the entering values and excludes predictor from the stepwise model if it does not satisfy the excluding threshold.

- The algorithm keeps on going until no variable can be added or excluded.

You can perform the algorithm with the function ols_stepwise() from the olsrr package.

ols_stepwise(fit, pent = 0.1, prem = 0.3, details = FALSE) arguments: -fit: Model to fit. Need to use `lm()`before to run `ols_stepwise() -pent: Threshold of the p-value used to enter a variable into the stepwise model. By default, 0.1 -prem: Threshold of the p-value used to exclude a variable into the stepwise model. By default, 0.3 -details: Print the details of each step

⚠️ Package note: recent versions of olsrr renamed these functions. Use ols_step_all_possible() in place of ols_all_subset() and ols_step_both_p() in place of ols_stepwise(). The arguments and the output are unchanged.

Before that, we show you the steps of the algorithm. Below is a table with the dependent and independent variables:

| Dependent variable | Independent variables |

|---|---|

| mpg | disp |

| hp | |

| drat | |

| wt | |

| qsec |

Start

To begin with, the algorithm starts by running the model on each independent variable separately. The table shows the p-value for each model.

## [[1]] ## (Intercept) disp ## 3.576586e-21 9.380327e-10 ## ## [[2]] ## (Intercept) hp ## 6.642736e-18 1.787835e-07 ## ## [[3]] ## (Intercept) drat ## 0.1796390847 0.0000177624 ## ## [[4]] ## (Intercept) wt ## 8.241799e-19 1.293959e-10 ## ## [[5] ## (Intercept) qsec ## 0.61385436 0.01708199

To enter the model, the algorithm keeps the variable with the lowest p-value. From the above output, it is wt

Step 1

In the first step, the algorithm runs mpg on wt and the other variables independently.

## [[1]] ## (Intercept) wt disp ## 4.910746e-16 7.430725e-03 6.361981e-02 ## ## [[2]] ## (Intercept) wt hp ## 2.565459e-20 1.119647e-06 1.451229e-03 ## ## [[3]] ## (Intercept) wt drat ## 2.737824e-04 1.589075e-06 3.308544e-01 ## ## [[4]] ## (Intercept) wt qsec ## 7.650466e-04 2.518948e-11 1.499883e-03

Each variable is a potential candidate to enter the final model. However, the algorithm keeps only the variable with the lower p-value. It turns out hp has a slightly lower p-value than qsec, so hp enters the final model.

Step 2

The algorithm repeats the first step but this time with two independent variables in the final model.

## [[1]] ## (Intercept) wt hp disp ## 1.161936e-16 1.330991e-03 1.097103e-02 9.285070e-01 ## ## [[2]] ## (Intercept) wt hp drat ## 5.133678e-05 3.642961e-04 1.178415e-03 1.987554e-01 ## ## [[3]] ## (Intercept) wt hp qsec ## 2.784556e-03 3.217222e-06 2.441762e-01 2.546284e-01

None of the remaining candidates has a p-value below the entry threshold. The algorithm stops here, and this is the final model:

## ## Call: ## lm(formula = mpg ~ wt + hp, data = df) ## ## Residuals: ## Min 1Q Median 3Q Max ## -3.941 -1.600 -0.182 1.050 5.854 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 37.22727 1.59879 23.285 < 2e-16 *** ## wt -3.87783 0.63273 -6.129 1.12e-06 *** ## hp -0.03177 0.00903 -3.519 0.00145 ** ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 2.593 on 29 degrees of freedom ## Multiple R-squared: 0.8268, Adjusted R-squared: 0.8148 ## F-statistic: 69.21 on 2 and 29 DF, p-value: 9.109e-12

You can use the function ols_stepwise() to compare the results.

stp_s <-ols_stepwise(fit, details=TRUE)

Output:

The algorithm finds a solution after two steps and returns the same output as the manual walkthrough above.

The final model is therefore explained by two predictors and an intercept: miles per gallon is negatively related to both gross horsepower and weight.

## You are selecting variables based on p value... ## 1 variable(s) added.... ## Variable Selection Procedure ## Dependent Variable: mpg ## ## Stepwise Selection: Step 1 ## ## Variable wt Entered ## ## Model Summary ## -------------------------------------------------------------- ## R 0.868 RMSE 3.046 ## R-Squared 0.753 Coef. Var 15.161 ## Adj. R-Squared 0.745 MSE 9.277 ## Pred R-Squared 0.709 MAE 2.341 ## -------------------------------------------------------------- ## RMSE: Root Mean Square Error ## MSE: Mean Square Error ## MAE: Mean Absolute Error ## ANOVA ## -------------------------------------------------------------------- ## Sum of ## Squares DF Mean Square F Sig. ## -------------------------------------------------------------------- ## Regression 847.725 1 847.725 91.375 0.0000 ## Residual 278.322 30 9.277 ## Total 1126.047 31 ## -------------------------------------------------------------------- ## ## Parameter Estimates ## ---------------------------------------------------------------------------------------- ## model Beta Std. Error Std. Beta t Sig lower upper ## ---------------------------------------------------------------------------------------- ## (Intercept) 37.285 1.878 19.858 0.000 33.450 41.120 ## wt -5.344 0.559 -0.868 -9.559 0.000 -6.486 -4.203 ## ---------------------------------------------------------------------------------------- ## 1 variable(s) added... ## Stepwise Selection: Step 2 ## ## Variable hp Entered ## ## Model Summary ## -------------------------------------------------------------- ## R 0.909 RMSE 2.593 ## R-Squared 0.827 Coef. Var 12.909 ## Adj. R-Squared 0.815 MSE 6.726 ## Pred R-Squared 0.781 MAE 1.901 ## -------------------------------------------------------------- ## RMSE: Root Mean Square Error ## MSE: Mean Square Error ## MAE: Mean Absolute Error ## ANOVA ## -------------------------------------------------------------------- ## Sum of ## Squares DF Mean Square F Sig. ## -------------------------------------------------------------------- ## Regression 930.999 2 465.500 69.211 0.0000 ## Residual 195.048 29 6.726 ## Total 1126.047 31 ## -------------------------------------------------------------------- ## ## Parameter Estimates ## ---------------------------------------------------------------------------------------- ## model Beta Std. Error Std. Beta t Sig lower upper ## ---------------------------------------------------------------------------------------- ## (Intercept) 37.227 1.599 23.285 0.000 33.957 40.497 ## wt -3.878 0.633 -0.630 -6.129 0.000 -5.172 -2.584 ## hp -0.032 0.009 -0.361 -3.519 0.001 -0.050 -0.013 ## ---------------------------------------------------------------------------------------- ## No more variables to be added or removed.

Linear Regression in R: Key Takeaways and Function Reference

- Linear regression answers a simple question: can you measure an exact relationship between one target variable and a set of predictors?

- The Ordinary Least Squares method finds the parameters that minimize the sum of the squared errors, that is the vertical distance between the predicted y values and the actual y values.

- The probabilistic model that includes more than one independent variable is called multiple regression models.

- The purpose of Stepwise Linear Regression algorithm is to add and remove potential candidates in the models and keep those who have a significant impact on the dependent variable.

- Variable selection is an important part of fitting a model, and stepwise regression performs that search automatically.

Every function used in this tutorial is listed below:

| Library | Objective | Function | Arguments |

|---|---|---|---|

| base | Compute a linear regression | lm() | formula, data |

| base | Summarize model | summary() | fit |

| base | Extract coefficients | lm()$coefficient | |

| base | Extract residuals | lm()$residuals | |

| base | Extract fitted value | lm()$fitted.values | |

| olsrr | Run stepwise regression | ols_stepwise() | fit, pent = 0.1, prem = 0.3, details = FALSE |

Note: Remember to convert categorical variables into factors before fitting the model.