Expanded Accounting Equation with Income & Expense

⚡ Smart Summary

Expanded Accounting Equation is the advanced version of the basic accounting equation. It adds Expenses and Drawings to the debit side and Revenue to the credit side, giving Assets + Expenses + Drawings = Liabilities + Revenue + Owner’s Equity, explained with worked examples.

Remember in tutorial 2 we learned the basic form of the accounting equation as:

Assets = Liabilities + Owners Equity

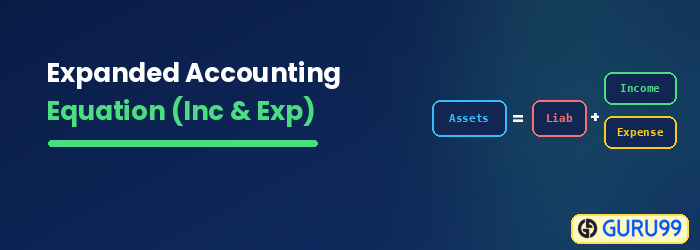

What is the Expanded Accounting Equation?

Expanded Accounting Equation is the advance version of basic accounting equation. It add accounts like Revenue, Expense and Drawings to the Equation.

Now that we also understand the terms Revenue, Expense, and Drawings, we can finally understand the accounting equation in its complete form. Let’s take a look.

Assets + Expenses + Drawings = Liabilities + Revenue + Owners EquityIn tutorial 2 we learned that the left side is known as the debit side and the right side is known as the credit side. The same rules apply here, only now we have some new additions to each side.

The Debit Side

The debit side now consists of not only Assets but also Expenses and Drawings.

The Credit Side

The credit side now consists not only of Liabilities and Owners Equity but also Revenue.

Let’s look at some common problems that might occur in your day to day business, and how they are recorded in the accounting equation.

Example 1: Purchasing a car with cash

Step 1: Identify the accounts involved in the transaction

Let’s identify the two accounts involved in this transaction.

- Bank – an Asset ( you will draw money to pay for the car)

- Car – an Asset (car will give you benefit for more than one year and is an asset)

Step 2: Determine where the accounts lie on Debit/ Credit Side

Both the accounts lie on the left-hand side of the equation.

Step 3: Determine which accounts will increase or decrease

So in order to balance the equation, one asset must increase (Car) and other must decrease (Bank).

| Debit side | Credit side | |||||

|---|---|---|---|---|---|---|

|

Assets |

Expenses |

Drawings |

= |

Liabilities |

Revenue |

Owner’s Equity |

|

Increase |

||||||

|

Decrease |

||||||

Example 2: Receiving revenue for selling Cakes

Step 1: Identify the accounts involved in the transaction

Let’s identify the two accounts involved in this transaction.

- Bank – an Asset ( you will deposit your revenue money into Bank)

- Cake Sales – aRevenue account

Step 2: Determine where the accounts lie on Debit/ Credit Side

In this case the 2 accounts lie on the opposite sides of the accounting equation.

Step 3: Determine which accounts will increase or decrease.

Both the accounts could increase or decrease.

But, it will never be the case that one account is increasing and other decreasing, otherwise the equation will not balance.

In this scenario, money from cake sale will be deposited in the bank. So Assets will increase. Likewise, Revenues will increase as well.

| Debit side | Credit side | |||||

|---|---|---|---|---|---|---|

|

Assets |

Expenses |

Drawings |

= |

Liabilities |

Revenue |

Owner’s Equity |

|

Increase |

Increase |

|||||

Exercises 3: Paying expenses with cash

| Debit side | Credit side | |||||

|---|---|---|---|---|---|---|

| Assets | Expenses | Drawings | = | Liabilities | Revenue | Owner’s Equity |

|

|

|

|

|

|

|

|

Example 4: Owner invests money in the business

| Debit side | Credit side | |||||

|---|---|---|---|---|---|---|

| Assets | Expenses | Drawings | = | Liabilities | Revenue | Owner’s Equity |

|

|

|

|

|

|

|

|

Example5: Owner withdraws money

| Debit side | Credit side | |||||

|---|---|---|---|---|---|---|

| Assets | Expenses | Drawings | = | Liabilities | Revenue | Owner’s Equity |

|

|

|

|

|

|

|

|

Example 6: Pay back a loan

| Debit side | Credit side | |||||

|---|---|---|---|---|---|---|

| Assets | Expenses | Drawings | = | Liabilities | Revenue | Owner’s Equity |

|

|

|

|

|

|

|

|

Notice every time the equation balances. If a debit account increases, then another debit account decreases. There will never be a time when two debit accounts increase because then the equation won’t balance!

Similarly, it’s also common to see a debit account increase and then a credit account increase with it. This also allows the equation to balance. You will never see a debit account increase and a credit account decrease because the equation will be left out of balance.

The equation is basic maths you learned at school!

1 = 1

If you add 5 to one side, we have to add 5 to the other side, Otherwise it will simply be wrong:

1+5 = 1

Wrong!

Or, we can get minus 5 from the same side to keep it balanced.

1+5-5 = 1

Don’t let the debits and credits confuse you. it’s all good ol’ pluses and minuses.

If you’re still not quite getting it, don’t worry. In the following tutorial, we’ll look at some problems of recording transactions to get some practice at using the full accounting equation.