SAP Credit Management Tutorial: OVA8

⚡ Smart Summary

Credit management in SAP SD lets a company sell on credit while controlling risk with a credit limit; when open orders exceed the limit, the order is blocked. This resource explains the credit checks and how to set them up.

SAP Credit Management

Credit management is a process in which a company sells a product or service to customers on a credit basis, collecting payment at a later time, after the sale. The amount of credit that a company fixes for a customer is called the credit limit. A customer can purchase from the company within the credit limit, and when the credit limit is crossed, the order is blocked by the system.

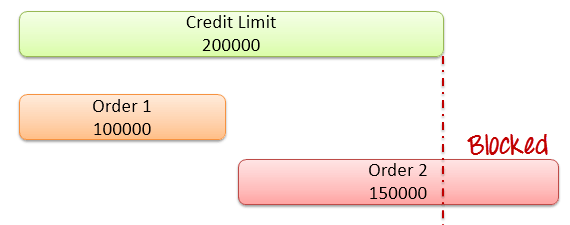

Example — Consider a company that creates a credit limit of 200,000 for a customer. The customer can buy on credit until that limit is reached. Suppose the customer places Order #1 for 100,000 and then Order #2 for 150,000. Now the total open order value crosses the credit limit, so Order #2 is blocked by the system because the credit limit has been reached.

Here the customer has ordered a total of Rs. 2,50,000 while the credit limit is Rs. 2,00,000, so Order #2 exceeds the limit and is blocked. The credit limit can be different for each customer.

Types of Credit Management in SAP SD

SAP SD offers two ways to check a customer’s credit:

1. Simple credit check: The simple credit check compares the value of all open items plus the value of the current sales order against the credit limit. (Open items are invoices for which the company has not yet received payment.)

2. Automatic credit check: The automatic credit check evaluates a transaction based on the customer’s credit rating and ensures the document is processed appropriately. The check runs automatically when you save the document, or when you choose Check Credit. Automatic credit checks are of two types:

- Static credit check — checks the credit limit against the total value of open sales orders, open deliveries not yet invoiced, and open billing documents not yet passed to accounting.

- Dynamic credit check — checks the same values, but only counts open order values that fall within a defined credit horizon, together with billed amounts that are not yet paid.

Static vs Dynamic Credit Check

Both the static and dynamic credit checks are types of automatic check, but they treat open sales orders differently. The table below compares them.

| Basis of comparison | Static credit check | Dynamic credit check |

|---|---|---|

| Open orders counted | All open orders, regardless of date | Only orders within the credit horizon |

| Time horizon | Not used | Uses a credit horizon, maintained in FD32 |

| Credit exposure | One combined figure | Split into a static part and a dynamic open-order part |

| Effect | Stricter; every open order adds to exposure | More flexible; far-future orders are excluded |

| Best for | Tight credit control | Businesses with long-dated orders |

In short, the dynamic check adds a time horizon so that orders scheduled far in the future do not consume the credit limit today, while the static check counts every open order at once. Because the credit horizon is set per customer in FD32, two customers on the same automatic check can behave differently, which lets a business tune credit control to each account’s risk profile.

How to Set Up Credit Management in SAP (OVA8)

Automatic credit control is configured in transaction OVA8 for the combination of credit control area, risk category, and credit group.

Step 1) Set the credit check.

- Enter T-code OVA8 in the command field.

- Click on the New Entries button.

Step 2)

- Enter the Credit Control area.

- Check the Credit Check option.

- Enter the credit limit validity period.

- Check the Static option.

- Check open orders and open deliveries.

Step 3) Click on the Save button.

Key Transaction Codes for Credit Management

Beyond OVA8, credit management uses a small set of transactions to set limits and release blocked documents. The most useful are:

- OVA8 – Automatic credit control: Defines the credit checks per credit control area, risk category, and credit group.

- FD32 – Customer credit master: Sets the credit limit and the credit horizon for a customer.

- OB45 – Credit control area: Defines the credit control area itself.

- OVAK – Assign credit check to sales document types: Controls which order types are checked.

- VKM1 / VKM3 – Blocked documents: List the sales documents blocked for credit so that finance can review and release them.

Together, these transactions let you define the credit rules, set each customer’s limit, and manage the documents that the checks block. In practice, a consultant configures OB45 and OVA8 once during setup, sets each customer’s limit in FD32, and then the finance team works mainly in VKM1 or VKM3 to review and release blocked orders day to day.